INTERVIEW

Falconstar Investments

Apr 15, 2021 · 7 min read

Exclusive Interview with Maulik Parekh on Investment Philosophy & Strategy

Investments & Portfolio with Maulik Parekh

Interviewer — What is your Investment Philosophy & Strategy?

Background & Learning:

In a manner of speaking, I would say my journey into the world of investments started way before I was even born. Family members from both my mother’s and father’s side were engaged in the investments business since the inception of the hallowed Bombay Stock Exchange. While I was growing up, investment was a dinner table discussion, although as a child it felt like making sense of an elephant by touching merely its tail. The intellectual curiosity to learn more about the markets was ingrained in me at a rather early stage in life. The passion for markets was fuelled by the bull run of the early 90s — also known as the Harshad Mehta Bull Run — when fortunes were made and lost.

Upon completing my Masters degree in Industrial Engineering, I was working in the US and during this period I studied the work of some of the most successful investors in the world, including the likes of Warren Buffett, Ben Graham and Peter Lynch. I realized that the Investing world comes full circle with growth, value and distressed styles of Investments. During different stages of economic and market cycles, there are different asset classes that outperform. There is also a perspective on broad based diversification to be gained from the new world, multi-strategy, Institutional Investors like Mr. Ray Dalio.

To sum it up, my Investment Philosophy is influenced by western thought leadership in the field of investing, which is to use a combination of growth and value style of investing.

Investment Philosophy:

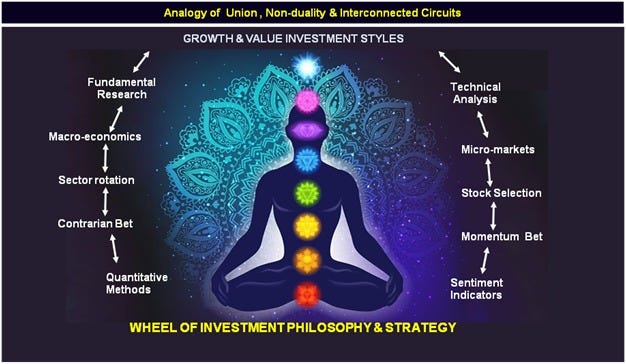

Investments have to be evaluated in the light of complex parameters like macro-environment, central bank actions, geo-political risks and business cycles. According to me, value and growth are two sides of the same coin. While Value investors are more disciplined in terms of identifying stocks precisely below their intrinsic valuations, the growth investors take a leap of faith by betting on the future growth prospects of a company in their computations. However, there is no denying the common thread between a long time horizon of Investment and the power of compounding. The idea is to take advantage of the information technology revolution, being sector and market cap agnostic; and identifying sustainable global companies that have competitive advantage with multi-bagger potential.

The ultimate goal is to buy such a stock at a price cheaper than its intrinsic value, which is in turn based on predictable earnings and growth trajectory modeling. This estimated intrinsic valuation and number of stocks in the portfolio has to strike a balance between the power of concentrating risk and benefits of diversification.

Wheel of Investment Philosophy and Strategy

Investment Strategy:

I follow a 25 years old, time tested and scientifically designed multi-strategy approach to Equity Portfolio Management for generating superior risk reward. This structured approach has 4 distinct phases to the Investment decision-making: (1) What to Buy? (2) How much to buy? (3) When to Buy? and (4) When to Sell?

The icing on the cake for Falconstar’s investment strategy is a technical trading overlay on top of three fundamentally oriented multi-cap stock portfolio strategies. One would say this hybrid mode is Falconstar’s x-factor, which generates Alpha using the multi-strategy approach and packaging it using quantitative portfolio risk management parameters.

Interviewer — What are your current views on the Markets?

I have been following the financial markets closely for the past 25 years and can say this, based on my experience. We have been witnessing unprecedented printing of money by central banks across the world, since 2009. But 2015 onwards, the markets have been decoupled from fundamental valuations and the situation only seems to further exacerbate.

Indian Markets:

My view on the Indian Equity markets is constructive, from a medium-to-long term perspective. As India achieves the goal of touching a GDP of $5 Trillion, it has potential to clock double digit 10%+ GDP growth for 10 years to come. If that happens, there are more than 50 consumer-facing B2C companies in India who will be key beneficiaries, and will consistently clock 3X of GDP growth for the coming decade. India will continue to be an indigenous consumer demand driven market for the next couple of decades because of the large demographic dividend in terms of low per capita GDP of USD 2000 and a young population of 35 years with a lifestyle focused on demand growth.

Although the current P/FCFE Ratio for NIFTY50 of greater than 35 leaves much to be desired from a valuation perspective, a meaningful correction is not materializing because of global and local factors. Global liquidity combined with the lack of participation froth in domestic markets is preventing a correction from fructifying. In the short term (3–12 months) if there is a bout of 2-Sigma or 15–20% correction, it should be used to buy on dips with a 5 year horizon.

Global Markets:

Global brands and Technology companies (NASDAQ:FANG) in the form of Nasdaq 100 will continue to flourish in the developed markets like the US. In the coming decades, Nasdaq100 Index should have a higher share of Biotech-Pharma firms compared to the current 10% because Bio-pharma has potential to emerge as the new Tech in the next 25 years.

While the US continues to be a global economic powerhouse, the Chinese economy will try to outstrip the US economy by 2040. Chinese financial markets will endeavour for greater global financial clout. Chinese stock markets will play significant catch-up with a Market cap / GDP of ~70% compared to US Market cap / GDP of 150%.

Talking about the current market cycle since 2009, the US Federal Reserve having indicated that they will maintain dovish stance till 2023, it is clear that only a geo-political event can spoil the party in Equity markets in 2021. We continue to be merry in the “last dance” stage of Financial Markets frenzy which are leading to frothy valuations, volumes and market participation. The inflationary pressure is likely to increase going forward, with no clear timeline when an economic shock could correct the market cycle. However, when it does, there is a distinct possibility of a “lost decade” like the case of deflationary Japanese economy in the 1990s. While history repeats itself in different forms, the next big bear market correction might happen because of sovereign default, unlike the e-commerce bubble of 2000 or the subprime credit crisis of 2009.

“Luck is what happens when opportunity meets preparation”. says Maulik Parekh

Interviewer — What Investment strategy should Indian Investors adopt in the post-Covid world.

The fundamentals of Investing haven’t changed during the dot com, GFC, or subprime crises. The same applies to Covid as well. It pays to be greedy when the markets are fearful. Like the previous Financial crises, Covid hit the world markets with an element of surprise. The quantitative trading systems worldwide further exacerbated the sharp correction in markets. For any six-sigma event like Covid, it takes time for any Investor to figure out when to call the bottom, because the bottom could be hit in waves. Normally, one event has a snowball effect on another, which eventually leads to a black swan crisis. However, as the saying goes, “Luck is what happens when opportunity meets preparation”. Seeing the light at the end of the tunnel, there was a clear indication that Technology and Healthcare are 2 key beneficiary sectors post-Covid from a thematic perspective.

The fundamentals of Investing haven’t changed during the dot com, GFC, or subprime crises. The same applies to Covid as well. It pays to be greedy when the markets are fearful. Like the previous Financial crises, Covid hit the world markets with an element of surprise. The quantitative trading systems worldwide further exacerbated the sharp correction in markets. For any six-sigma event like Covid, it takes time for any Investor to figure out when to call the bottom, because the bottom could be hit in waves. Normally, one event has a snowball effect on another, which eventually leads to a black swan crisis. However, as the saying goes, “Luck is what happens when opportunity meets preparation”. Seeing the light at the end of the tunnel, there was a clear indication that Technology and Healthcare are 2 key beneficiary sectors post-Covid from a thematic perspective.